How High Net-Worth Women Can Optimize Their Gifting Strategies

November 16, 2020

How to Retire in a Recession

December 4, 2020

“One cannot ride a horse backwards and still hold its reins.” – Richard Paul Evans

One year ago we wrote a newsletter, with the same title, that explained why it may not make sense to chase an asset class that has done well recently (namely U.S. equities rather than international or emerging market stocks). This “recency” phenomenon, or short-term track record investing, can come back to haunt investors who think that just because something did well yesterday means it will do well tomorrow. In other words, “past performance is no indication of future results”.

To drive the point home, we borrowed research from Dimensional Fund Advisors that showed not just the last few years results, but more appropriately the last twenty years results – which we believe is a much better perspective since the short term (be it a few days, a few months, or even a few years) can be so transitory. Similarly, we will again use Dimensional’s research to explain why it may not make sense to chase the biggest stocks that everyone seems to be enamored with right now and those which seem to only go up recently, pandemic or not.

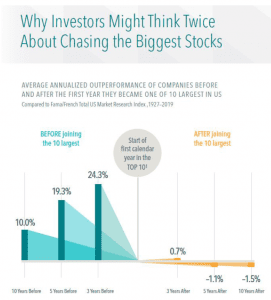

Accordingly, please see the graph on the next page. Simply put, it shows that as companies grow and become some of the largest firms trading on the U.S. stock market, the impressive returns that push them to that achievement can be fleeting. In fact, not long after becoming one of the top ten (“Top 10”) largest companies by market capitalization, these stocks tend to lag the market thereafter.

Research shows that, from 1927 to 2019, the average annualized return for these stocks over the three years prior to joining the Top 10 was nearly 25% higher than the market. However, their edge was only 1% better in the three years after they joined the Top 10.1 And just five years after joining the Top 10, these stocks, on average, underperformed the market – a stark turnaround from their earlier advantage. Ten years out and they underperformed by an even wider gap!

So, please never forget that the phrase “past performance is no indication of future results” is not just a simple industry disclaimer, but a researched truism as well. And by chasing yesterday's winner, you may only be increasing your chances of finding tomorrow’s loser.

Last but not least, we hope you have a wonderful and Happy Thanksgiving. And though we may be in the midst of bizarre and depressing days, being grateful for every day, every friend, and every family member is what will get us through these tough times to see better days. Take care!

Past performance is no guarantee of future results. Indices are not available for direct investment; therefore, their performance does not reflect the expenses associated with the management of an actual portfolio. This information is intended for educational purposes and should not be considered a recommendation to buy or sell a particular security. Named securities may be held in accounts managed by Dimensional.

Source: Dimensional, using data from CRSP. Includes all US common stocks excluding REITs. Largest stocks identified at the end of each calendar year by sorting eligible US stocks on market capitalization. Market is represented by the Fama/French Total US Market Research Index. Annualized Excess Return is the difference in annualized compound returns between the stock and the market over the 3-, 5-, and 10-year periods, before and after each stocks’ initial year-end classification in the top 10. 3-, 5-, and 10-annualized returns are computed for companies with return data available for the entire 3-, 5-, and 10-year periods respectively. The number of firms included in measuring excess returns prior (subsequent) to becoming a top 10 stock consists of 38 (53) for 3-year, 37 (52) for 5-year, and 29 (47) for 10-year. Fama/French Total US Market Research Index: The value-weighed US market index is constructed every month, using all issues listed on the NYSE, AMEX, or Nasdaq with available outstanding shares and valid prices for that month and the month before. Exclusions: American Depositary Receipts. Sources: CRSP for value-weighted US market return. Rebalancing: Monthly. Dividends: Reinvested in the paying company until the portfolio is rebalanced. Eugene Fama and Ken French are members of the Board of Directors of the general partner of, and provide consulting services to, Dimensional Fund Advisors LP. Dimensional Fund Advisors LP is an investment advisor registered with the Securities and Exchange Commission.

{kind=link}

{kind=link}

{kind=link}